Kansas is relearning a lesson it should already know: the problem is not revenue. The problem is spending discipline. That is the real issue behind the current budget debate.

The House budget for fiscal year 2027 would spend nearly $27 billion in total funds and almost $11 billion from the State General Fund, while the Senate version totals $26.8 billion in total and $10.8 billion from the General Fund. These amounts may sound routine in the Capitol, but they should concern every Kansas taxpayer.

Kansas has many of the right ideas on paper. The state has talked for years about accountability, performance, and fiscal responsibility. It even put performance-based budgeting into law in 2016. The problem is that these reforms are too often admired, discussed, and then ignored. Agencies still come in with requests, lawmakers still make marginal adjustments, and last year’s budget still acts as the starting point for this year’s growth. That is not reform. That is autopilot with committee hearings.

Kansas has been down this road before. The mistake a decade ago was not cutting taxes. The mistake was attempting tax relief without first fixing the spending side. When the fiscal pressure hit, the government was protected, taxes were blamed, and the wrong lesson was written into the political memory. That history matters now because the same pattern is reappearing: leaders talk about stability while preserving an inflated budget baseline built during and after the pandemic surge.

This is why Kansas needs to return to a simple rule: responsible spending should grow no faster than what is needed to efficiently provide necessary services and that taxpayers can afford.

Long-Term Spending Growth in Kansas

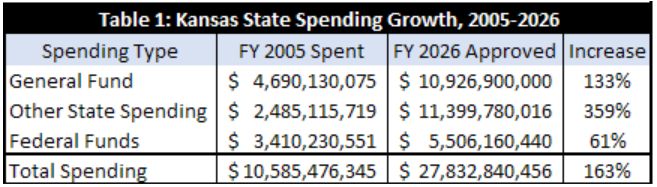

The updated budget data, shown in Table 1, highlight how far spending has drifted from sustainable levels. From fiscal year 2005 to fiscal year 2026, total Kansas state spending increased from $10.6 billion to $27.8 billion, a 163 percent increase.

These figures highlight a key point: Kansas spending growth has been driven primarily by expansions in non-general-fund programs and other state spending categories.

Spending from state funds jumped from $7.2 billion in 2005 to $22.3 billion now. Are Kansas taxpayers getting a lot of new services now that weren’t provided in 2005, or are they getting the same basic services at vastly higher costs?

Spending Growth Far Exceeds Sustainable Levels

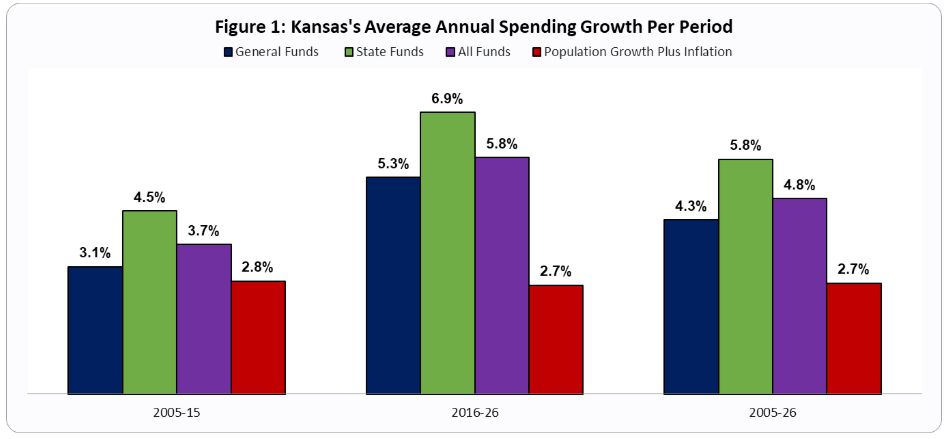

While population growth and inflation place natural limits on the average taxpayer’s ability to fund the government, Figure 1 highlights how government spending in Kansas has grown much faster than these economic factors.

Kansas first needs to work on reducing spending to pre-pandemic levels, rather than treating emergency-era growth as the new permanent floor. If lawmakers start from a bloated baseline, even a reasonable cap can ratify too much government spending.

The state’s own fiscal conditions make this more urgent, not less. The governor’s proposed fiscal year 2027 general fund budget spends roughly $640 million more than projected revenues, following a prior year budget that spent about $700 million more than the state collected. Supporters say current growth is modest, but that misses the point. The issue is not whether this year’s increase sounds small. The issue is that spending was never meaningfully reset after the temporary spike. Once the baseline rises, every subsequent budget is built on it.

The Cost of Overspending

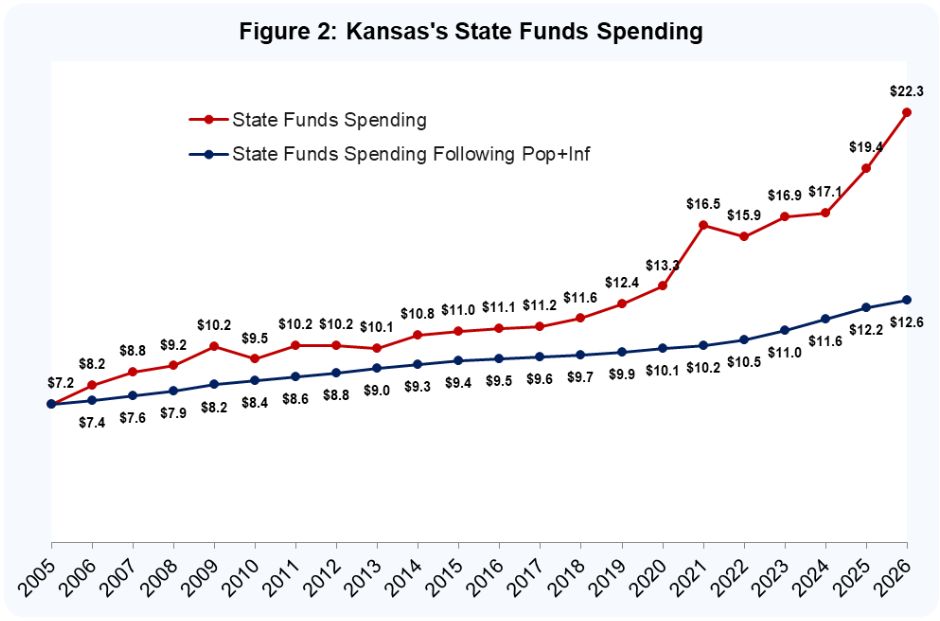

The consequences of this spending pattern become clear when comparing actual spending to what it would have been under a responsible budget path. If Kansas had limited spending growth to population growth plus inflation since 2005, state funds spending, which excludes federal funds, in 2026 would be $12.6 billion, rather than $22.3 billion, as shown in Figure 2.

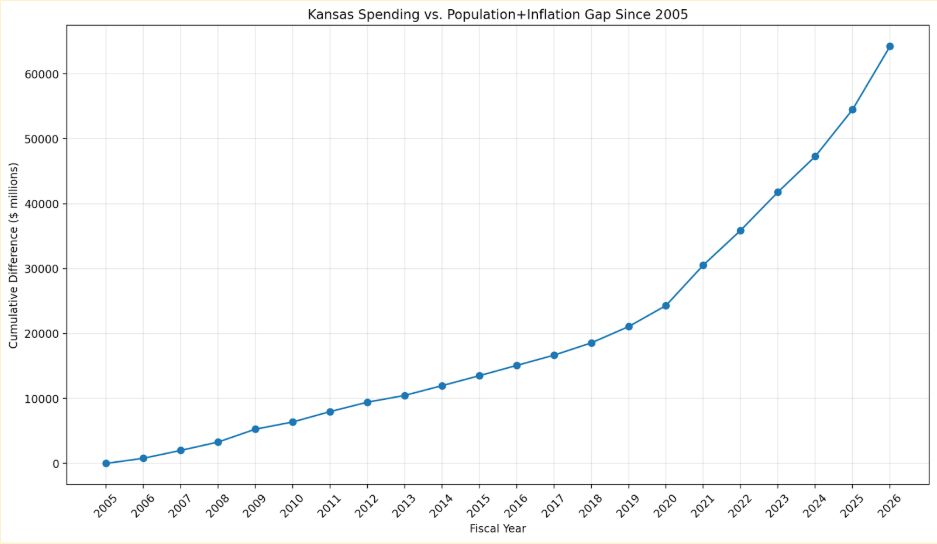

That means Kansas is currently spending roughly $10 billion more per year than it would have under a responsible growth path. Over time, that costly difference compounds dramatically. The cumulative gap between actual and responsible spending has exceeded $64 billion since 2005, as noted in Figure 3 below.

The $64 billion in excessive spending could have been returned to ( or never actually taken from), taxpayers in the last two decades if legislators followed the RKB path. Not only would the returns to taxpayers have been significant, spending still would have grown from $7.2 billion to $12.6 billion, for a 75 percent increase, instead of the increase from $7.1 billion to $22.3 billion, or a 210 percent increase.

A Responsible Path Forward

The purpose of the Responsible Kansas Budget is not to eliminate government services or force unrealistic cuts. Instead, it provides a simple fiscal rule to ensure the government grows at a sustainable pace. This approach will help avoid the problems of tax ratchet like during the last decade and provide a responsible budget path to allow taxes to be lowered.

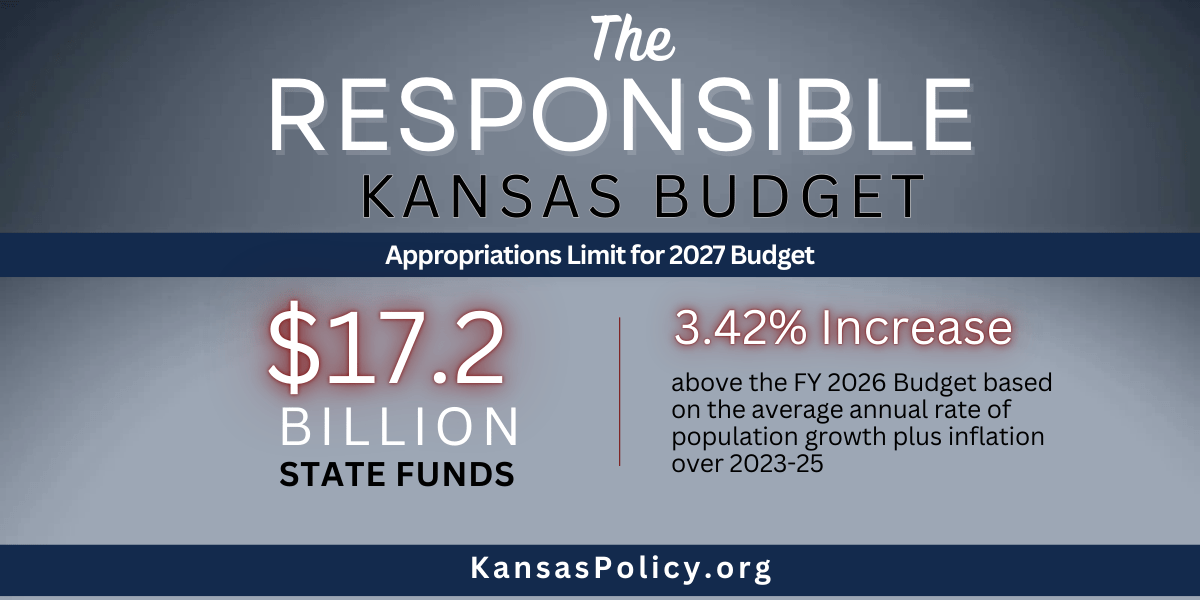

The rule is straightforward: Limit annual spending growth to population growth plus inflation. Applying that rule to current spending levels produces a recommended state funds spending limit of $23.09 billion for fiscal year 2027, compared with a 2026 base of $22.33 billion. This allows spending to grow modestly while restoring fiscal discipline.

However, given the substantial overspending over time, it is essential to reduce spending to the 2019 or 2020 levels (which was already $3 billion above population plus inflation),and then change spending by a maximum of population growth plus inflation thereafter. Using the three-year averages of population growth plus chained CPI inflation since then along with the latest increase of 3.42% from 2023 to 2025, the Responsible Kansas Budget for 2027 is $17.2 billion using 2020 as the base year. This is $10 billion less than what they are planning to appropriate for 2027.

Other sound budgeting ideas include the following.

First, enforce performance-based budgeting as intended. Programs should have measurable goals, and appropriations should depend on results rather than inertia. Second, pair that with what’s in law for zero-based budgeting, so agencies periodically justify their spending from the ground up instead of assuming automatic renewal. Third, make the interim budget review a real legislative function. Committees should spend the months after the session evaluating outcomes, duplication, and weak performance rather than waiting for agencies to return with another request for more money. The logic behind the regular examination of government effectiveness is straightforward: you do not get better government by reviewing it less often.

Kansas should also normalize independent efficiency audits and regular program evaluations. Internal review has an obvious flaw: agencies rarely recommend shrinking themselves. Outside scrutiny is much more likely to identify overlap, stale missions, and savings opportunities. That matters because every dollar wasted on weak programs is a dollar unavailable for core services or tax relief. Kansas does not need more internal reassurance. It needs more external accountability.

The payoff for doing this right is not just a tidier budget. It is a more competitive Kansas. Kansas is a middle-of-the-pack spender and tax collector, not a lean, low-tax state. Even when revenues beat projections, taxpayers often do not see relief because spending absorbs the excess first. That is exactly backward.

Finally, budget surpluses above a strict spending limit should be used to lower tax rates, not to expand the government’s permanent footprint. That is how Kansas can move toward a tax code that rewards work, investment, and growth.

Kansas does not need a new theory of budgeting. It needs the courage to follow the good rules it already has.