How property tax hikes squeeze affordability

Property taxes are a large and growing source of concern for many Minnesotans.

KSTP recently ran a story titled “Valuations up, sale prices down for some metro homeowners;” KAAL ran another titled “Minnesotans see significant increases in property value assessments,” which notes:

In LeRoy, a man named Harlan Olson said he’s now paying $1000 more in property taxes after the value of that property unexpectedly increased on a home that has remained the same for years.

“$238,600, that’s almost a $50,000 increase in one year,” Olson said.

Olson has lived in LeRoy since 2021 after moving his family from Adams. Between buying his home and land, the total cost was around $30,000 — nearly 90% less than what the county says his property is currently valued at just five years later.

“Now they’re saying this land according to them was valued at a quarter million dollars. Now how can that happen?” Olson said.

Between 2024 and 2025, Olson’s property value increased by $50,000 and has gone up another $20,000 this year despite no recent renovations. The increase is reflected in his property taxes.

“[They were] around 3000 last year. Now they’re right around 4000,” Olson said.

Property tax hikes are another source of the squeeze Minnesotans are feeling on the affordability of their lives. “According to the Minnesota Department of Revenue,” KAAL reports, “the certified property tax levies for all local governments in 2026 is nearly $14 billion — a 6.8% increase from last year.”

The process of setting property tax rates is rather opaque — perhaps by design — and it doesn’t help that local governments don’t do much to explain it. KAAL reports that “County assessors follow statewide practices when setting these property taxes. ABC 6 News reached out to multiple county assessors in our area, but none were available to discuss the property assessment process.”

The process basically works like this:

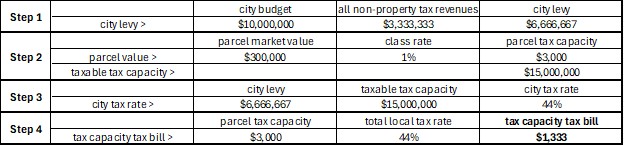

Step 1

First, as Dakota County outlines, “Each taxing district sets their levy.” As the League of Minnesota Cities explains:

Each year, the city, county, school district, and any special property taxing authorities must establish how much property tax they want to collect in the following year by Dec. 28.

For cities, the property tax levy is set after the consideration of all other revenues, including state aids like local government aid (LGA).

- That is: [city budget] – [all non-property tax revenues] = [city levy]

For many cities within the seven-county Twin Cities metropolitan and on the Iron Range, the levies are reduced by an amount of property tax revenue derived from the metropolitan and range area fiscal disparities programs.

Step 2

Second, as Dakota County puts it, “The tax rate is determined by spreading the levy over the tax base.” We have the levy from the previous equation. To calculate the tax base, the League of Minnesota Cities explains:

Assessors try to determine the approximate selling price of each parcel of property based on current market conditions.

A property class is also assigned to each parcel of property based on the use of the property. For example, property that is owner-occupied as a personal residence is classified as a residential homestead.

The classification is important because the Minnesota system assigns a weight to each class of property. Generally, properties associated with income production (e.g., commercial and industrial properties) have a higher classification weight than other properties.

The tax capacity of each parcel is a percentage of each parcel’s market value.

2) That is: [parcel market value] * [class rate] = [parcel tax capacity]

For example, a $75,000 home classified as a residential homestead has a class rate of 1.0% and therefore a tax capacity of $75,000 x .01 or $750.

Doing this for every property in the jurisdiction and adding the results together gives us the “taxable tax capacity,” or tax base.

Step 3

So now we have to spread the levy from Step 1 by the tax base from Step 2. The League of Minnesota Cities explains that:

The county calculates the city tax rate by dividing the city levy (minus the fiscal disparities distribution levy, if applicable) by the taxable tax capacity.

3) That is: [city levy] / [taxable tax capacity] = [city tax rate]. The tax rate is expressed as a percentage.

This same calculation is completed for the county based on the county’s levy and tax base, the school district, and all special taxing authorities. The sum of the tax rates for all taxing authorities that levy against a single property produces the total local tax rate. The county uses the total local tax rate to determine the overall tax burden for each parcel of property.

Step 4

Nearly there.

Finally, as Dakota County explains, “Your tax bill is calculated by multiplying your property’s taxable value by the total tax rate for your location.” “That is,” as the League of Minnesota Cities puts it:

4) [parcel tax capacity] * [total local tax rate] = [tax capacity tax bill]

The tax statement for each individual parcel itemizes the taxes for the county, municipality, school district, and any special taxing authorities.

To make this clearer, Table 1 lays out the process for a hypothetical town with 5,000 properties all of the same value:

Table 1: Hypothetical property tax calculation

But what really sends that property tax payment up and squeezes affordability for Minnesotans? We’ll look at that tomorrow.