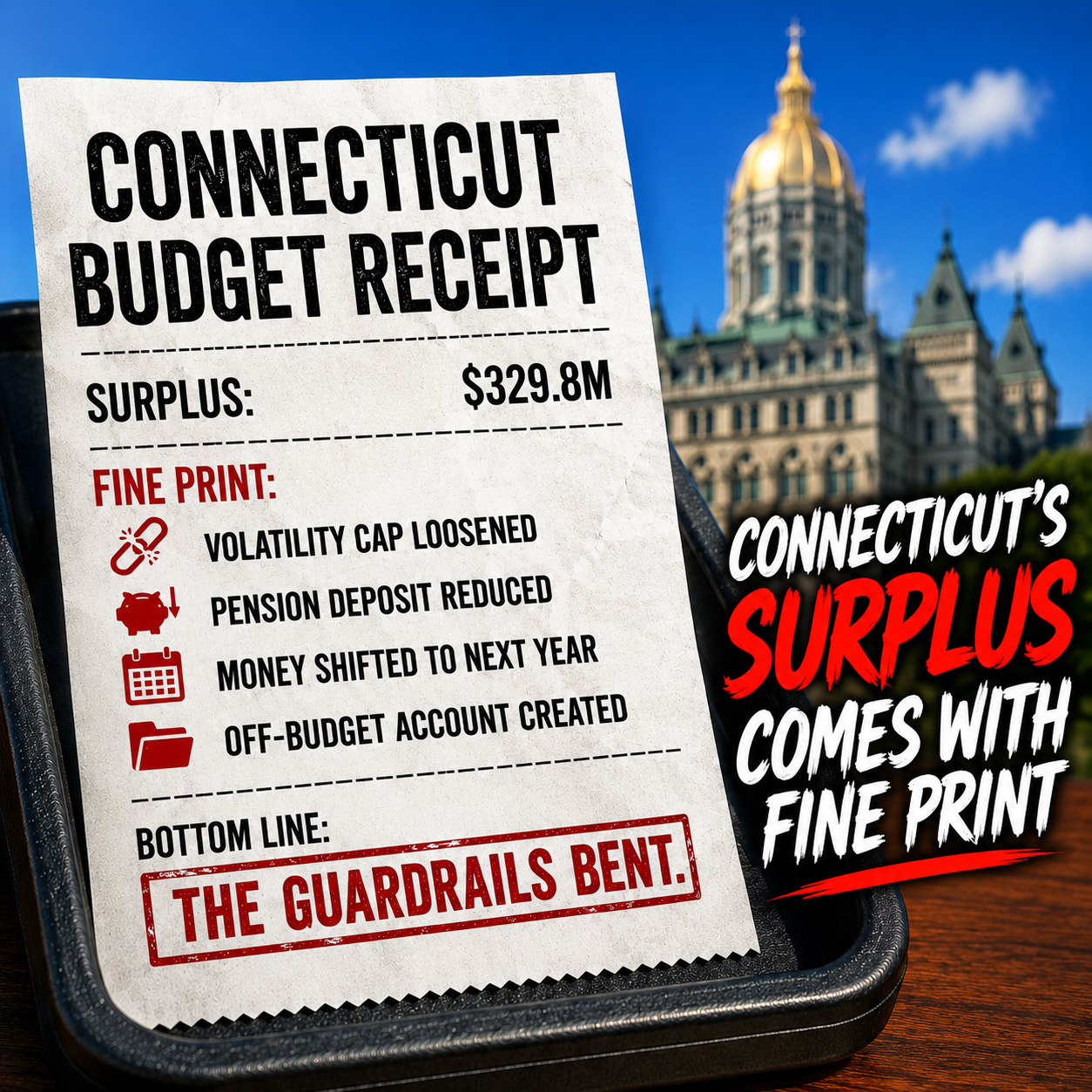

Connecticut lawmakers will point to the Office of Fiscal Analysis (OFA) May 28 reports as proof the state remains firmly in the black. The headline number is convenient: a projected $329.8 million General Fund surplus for FY 26. The fine print tells a more complicated story.

OFA’s May 28 budget projections, expenditure detail and revenue detail reports show Connecticut’s projected surplus depends heavily on policy changes enacted in the revised budget only days earlier. OFA states plainly that absent those changes, Connecticut would have ended FY 26 with a $45 million General Fund deficit. Instead, those mid-course adjustments by lawmakers produced a projected $329.8 million surplus, a swing of $374.8 million. The surplus is real — but it was built, not found.

The Guardrail That Got in the Way

Central to that construction was a temporary loosening of one of Connecticut’s most important fiscal reforms.

Connecticut adopted the volatility cap in 2017 to prevent lawmakers from treating unpredictable revenue as permanent spending. The mechanism requires unusually high collections from volatile tax sources, particularly estimated and final income-tax payments and the pass-through entity tax, to flow toward pension debt rather than ongoing spending. The logic is straightforward: Connecticut’s revenue depends heavily on capital gains, investment income and high-earner payments, all of which move sharply with markets. In good years, the excess is supposed to reduce long-term liabilities rather than finance current commitments.

This year, lawmakers temporarily raised the cap by $813.7 million for FY 26. The result, per OFA, is a smaller pension-debt payment: $1.13 billion instead of $1.86 billion, a reduction of roughly $726 million. Connecticut will still make a substantial contribution, but hundreds of millions of dollars that otherwise would have gone toward pension obligations are instead available for other uses.

The long-term cost is not theoretical. OFA estimates the change will reduce future pension-cost savings by $62.2 million a year beginning in FY 29. Annual savings projected at $159.3 million under the previous approach are now projected at $97.1 million.

That freed-up money helped fund several new or expanded spending items: $162.2 million for supplemental education grants, $100 million in municipal aid, $17.8 million for charter, magnet and vocational-agriculture schools, and $3 million for Department of Education administrative costs. The issue is not whether those items have merit. It is that money otherwise committed to pension debt was redirected to cover FY 26 spending, and that is precisely the habit the volatility cap was designed to prevent.

A Good Year in the Wrong Kind of Revenue

The revenue picture reinforces the concern. Corporation-tax receipts are projected to come in $422.8 million below budget, a 25.5 percent shortfall against a target of roughly $1.66 billion. Offsetting that gap is a surge in exactly the revenue the guardrails were designed to quarantine: estimated and final income-tax payments running $917.2 million above budget, and pass-through entity tax collections exceeding projections by roughly $450.3 million.

In other words, Connecticut benefited from a strong year in volatile, market-sensitive collections, and Hartford’s response was to temporarily relax the rule meant to stop politicians from spending that windfall as though it will recur.

Elsewhere in the Fine Print

The May 28 reports surface additional examples of fiscal maneuvering. The Special Transportation Fund shows a projected $30 million surplus for FY 26, but only after lawmakers moved $100 million into FY 27. Without that shift, the surplus would have been $130 million. The move does not strengthen the fund; it delays the next problem. OFA projects a significant operating deficit for the fund in FY 28.

The revised budget also shifts $963.3 million into a newly established off-budget Hospital Supplemental Payments Account in FY 27, a decision OFA says contributes to a smaller-than-anticipated Budget Reserve Fund deposit. Off-budget accounts are not inherently improper, but they make it harder for taxpayers to follow the true scope of state commitments.

The Temptation Problem

None of this means Connecticut is approaching fiscal collapse. The state’s budget position today is meaningfully stronger than it was a decade ago. That is precisely what makes the fine print worth examining.

Connecticut does not have a revenue problem so much as a temptation problem. A large pool of volatile revenue appeared, the fiscal rule got in the way, and Hartford found a way around it. That should concern taxpayers more than an honest deficit would. A deficit forces an admission that the math does not work. A surplus assembled this way allows lawmakers to claim fiscal responsibility while demonstrating that the rules are negotiable.

The guardrails were designed to protect Connecticut from exactly this pattern: treating good-year revenue as permanent, deferring hard choices and passing the long-term cost forward. If they can loosen them whenever the budget requires it, they are not guardrails. They are suggestions.