The most important point to understand regarding property taxes is that they are budget-driven. This simply means local taxing districts, which include counties, cities, schools, fire districts, etc., set property tax budgets, and those budgets are the primary driver of property tax payments and the changes (usually increases) over time. Long-term property tax relief requires budget restraints. There is no other sustainable long-term solution for reducing property taxes. We will explore all of the options (excluding amending the state constitution) on the table, but spending restraints at both the state and local levels are the cornerstone of property tax relief.

There are four ways to reduce property taxes. Some are general reductions, while others are carve-outs and shifts.

- Limit the ability of taxing districts to increase their budgets. As it stands now, state law prescribes limits on how much local units of government can increase property tax budgets each year. Currently, local units of government can increase their budgets by up to 3% plus a growth factor for new construction for an overall cap of 8%, with some exceptions. Therefore, one approach is to simply limit the increase to something less than 3% for the general increase and adjust the growth portion to reflect differentials for high-growth areas. This approach has had limited success because many of the roughly 1,000 taxing districts flood the Capitol with mayors, commissioners, fire officials, etc., to oppose any legislation imposing lower budget increase caps.

- Shift the tax burdens among different classes of taxpayers. This approach is politically popular (especially with local units of government) because there are more homeowners than commercial property owners, for example. Elected officials can placate homeowners by shifting burdens onto other taxpayers without reducing a dime of spending by taxing districts. This is not a good approach because burdening one group to help another is, by definition, redistribution. Perhaps a case can be made that one group is overburdened relative to another, but let’s look at some data that disproves this notion.

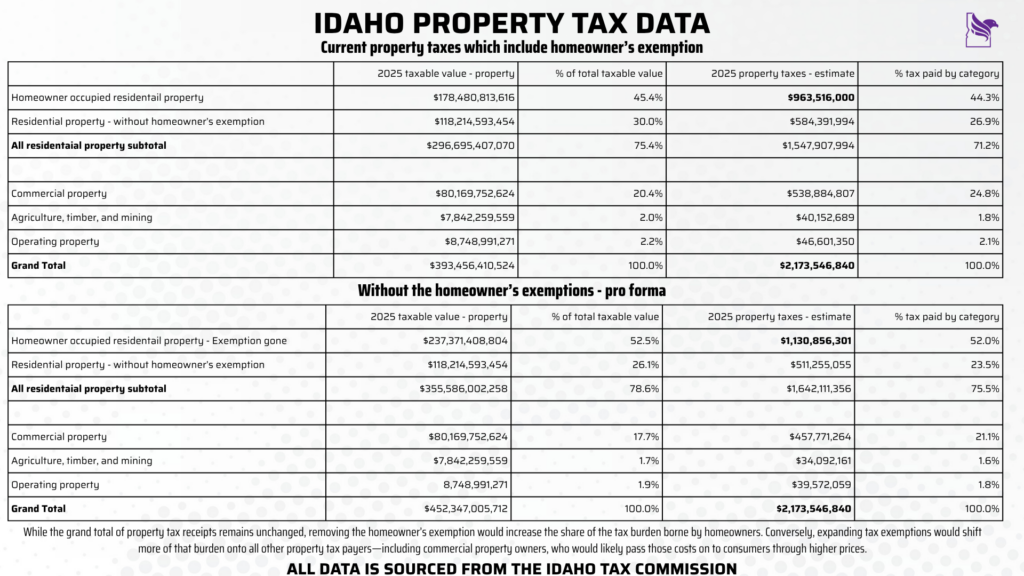

In the first table, we see property taxes as they are currently distributed and paid by broad categories. The top table shows the impact of both the homeowner’s exemption and the tax relief provided to homeowners directly and indirectly with House Bills 292 and 521. In the second table, based on tax commission projections, the homeowner’s exemption (currently capped at $125,000) is eliminated entirely. Note the following important points:

- Formerly exempt homeowners would see an overall increase of about 17%, even though the total property taxes levied do not change.

- Every other category of property taxpayers would see a decrease, even though the total property taxes levied do not change.

- Exempting some taxes for one group but not others is simply a shift; it may seem like a tax cut if you get the benefit of the exemption, but another property taxpayer is covering it.

- If the homeowner’s exemption increased from $125k to $175k, the primary residential homeowners would see a large decrease in property taxes, but every other category would absorb that decrease.

- Because not everyone has the same taxing districts on their property tax bill, the data presented above is the total impact for each category and does not imply that every individual in that category will see the same impact.

- Property taxes can be reduced for certain classes of taxpayers without reducing budgets by using funds outside property taxes. For example, using sales taxes to replace property taxes, as recent legislation (House Bills 292 and 521) has done. This is the preferred method for those who are afraid of offending the roughly 1,000 active taxing districts in Idaho by reducing their budgets. However, it is important to understand whether the use of sales tax funds is a carve-out or general tax relief. Carve-outs for tax relief have been made for certain veterans, senior citizens, the blind, and a few other categories, using what is called a “circuit breaker.” Currently, $24.5 million in sales taxes is used to provide “carve-out” relief without reducing the dollars that local units of government receive, because the state is picking up the tab. This document from the tax commission describes the circuit breaker in more detail. While many people would agree that blind people or disabled veterans deserve a break, where do we draw the line with carve-outs? If there were no property taxes, there would be no need for a carve-out because the blind, along with everyone else, would be paying zero.

- The final option combines the political advantages of option 3 with the broad approach of option 1. That is, to use sales taxes to displace property taxes entirely over a longer time horizon. For tax year 2025, recently passed legislation provided more than $300 million in tax relief to homeowners. It accomplished this by providing sales tax dollars to directly offset property taxes paid by homeowners. In addition, the local school district received sales tax dollars for facility funds to partially offset the need for additional levies. These are relatively small amounts compared to overall property taxes, budgeted at $2.5 billion. But they provide a template for continuing to use the growth in sales tax revenues to offset local property taxes. We have discussed this path in detail. Let’s address a couple of questions head-on. Wouldn’t using sales taxes to offset property taxes reduce the dollars available to fund the state government? Yes, it would, and that is a feature, not a bug. As we stated in the introduction, tax relief requires spending restraint. Secondarily, if local units of government were to get more sales tax dollars from the state, would it be reasonable to ask them to restrain spending? Of course it would. And the tradeoff would be freeing them from vexing their local taxpayers by constantly squeezing them for more money. This is a path forward that can work.

Here’s the bottom line. Property taxes are never going to go down unless and until two things happen: 1) Reverse the current trajectory of government spending growth! 2) Replace property taxes with tax collections from another source while being careful not to raise taxes elsewhere (Note: This, too, requires spending restraint).

IFF has carefully and consistently outlined how this can be done. For additional background reading on this subject, here is an earlier property tax explainer.

In addition, here is a good resource from the Idaho Tax Commission.