Calls to eliminate property taxes are echoing across the country, understandably generating tremendous enthusiasm among taxpayers and legislators. The desire is so intense that some Kansans are demanding the immediate elimination of property taxes.

Eliminating property taxes altogether, or even on a single property classification such as residential, requires careful consideration of the cascading implications of the various options. It’s not exactly Newton’s Third Law of Motion (when Object A exerts a force on Object B, Object B simultaneously exerts an equal and opposite force on Object A), but any change in tax policy alters economic behavior.

For example, at some point, higher taxes on gasoline, tobacco products, and alcohol prompt some people to cross a state line for those purchases. That’s not necessarily a reason to outright reject an idea, but the implications must be considered.

The purpose of this column is not to advocate for or against anything, but to provide information to help each taxpayer and legislator begin forming their own opinions.

There are about 15 billion valid reasons to call for the elimination of property tax. Property taxes statewide totaled $97.5 billion between 2005 and 2025. That total would be $82.6 billion if property taxes were increased to account for inflation and population growth, so local governments unnecessarily took $14.9 billion from taxpayers on that basis.

There are about 15 billion valid reasons to call for the elimination of property tax. Property taxes statewide totaled $97.5 billion between 2005 and 2025. That total would be $82.6 billion if property taxes were increased to account for inflation and population growth, so local governments unnecessarily took $14.9 billion from taxpayers on that basis.

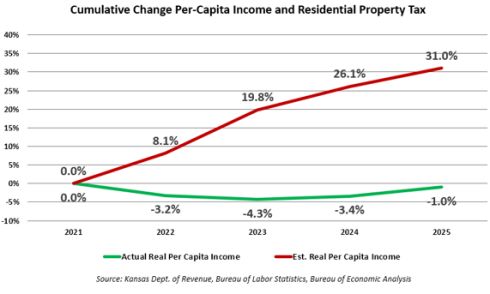

The average property tax on residential property jumped 31% over the last four years, while inflation-adjusted per capita income declined by 1% in Kansas. Meanwhile, legislators in the House and Senate haven’t been able to reach an agreement on a way to limit assessed valuation increases over the last three years.

There are many options to eliminate property taxes, each with side effects that legislators must examine to determine the trade-offs most voters are willing to accept. Replacing $7 billion in statewide property taxes that fund cities, counties, school districts, community colleges, and other local entities is a complex challenge that will likely require a combination of measures rather than a single solution.

Options to eliminate property taxes fall into two broad categories: replace the property tax with other revenue sources, or reduce government spending so that less revenue is needed. Simply increasing one tax to offset the reduction or elimination of another has little impact on the overall tax burden. The burden may shift up or down for some groups, but the overall burden in the state doesn’t change much, and that matters a lot to a state like Kansas, which is already very uncompetitive on taxation.

Increasing income tax rates rather than sales tax rates is not an economically viable option because income tax is the most destructive tax on the state’s economy. In “Reforming Kansas Tax Policy,” a paper jointly published by Kansas Policy Institute and the Economic Research Center at The Buckeye Institute, the authors explain that income taxes are the most harmful because they make less money available for people and businesses to spend and incentivize moves to states with more competitive income tax rates.

Kansas Senator Mike Murphy introduced SB 488 to replace property taxes with a 7.6% sales tax on purchases under $20 and a flat $1.60 fee on transactions over $20. The hearing at the Senate Tax Committee was packed with supporters, who were disappointed to hear Senator Murphy acknowledge that his plan was intended to start a conversation because, as he stated, it doesn’t work as written.

First of all, the data needed to set a surcharge that would generate enough additional sales tax doesn’t exist. Also, the state’s school funding formula would have to be rewritten to replace the multiple property tax sources that public schools collect.

There are at least seven options to generate new sales tax revenue in Kansas:

- A combination of an add-on percentage up to a certain purchase amount and a flat fee thereafter.

- Increase the local sales tax on all purchases, with each jurisdiction setting its own rate.

- Increase the state sales tax and distribute the additional proceeds to local taxing authorities.

- Add a flat fee to each transaction regardless of the purchase amount.

- Eliminate some or all sales tax exemptions.

- Some combination of options one through five.

- Establish a separate surcharge for each county to offset the total property taxes collected in each county.

It’s a near certainty that at least some of these options would create winners and losers. Some communities would get windfalls, while others would be shortchanged, because the data needed to do the calculations doesn’t exist. The Kansas Department of Revenue has sales tax revenue data for each jurisdiction, but no one tracks the number of transactions, making it impossible to determine how much a flat fee on each transaction would generate by community.

Many cities and counties have local sales tax rates that could be increased, but the rates needed to eliminate their property taxes would be rather high because property tax collections for the operation of cities, counties, and other municipalities are much higher than sales tax collections in most counties. In 2025, local sales and use tax collected for the operation of cities and counties totaled $1.7 billion, whereas those entities collected a little over twice as much – $3.5 billion – in property taxes. While property taxes collected by cities and counties averaged 2.1 times their sales tax, the median property tax multiplier is 4.6 times the sales tax.

Put differently, the local sales tax rates would need to be multiplied by a factor of five or more in half the state to generate enough sales tax to eliminate the property tax.

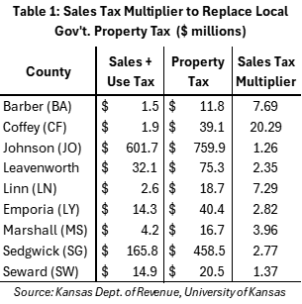

For example, Table 1 shows that local governments in Barber County collected 7.69 times as much property tax as sales tax ($11.8 million and $1.5 million, respectively). The multiplier is only 1.26 in Johnson County, but it is 20.29 in Coffey County, and a few others are higher.

For example, Table 1 shows that local governments in Barber County collected 7.69 times as much property tax as sales tax ($11.8 million and $1.5 million, respectively). The multiplier is only 1.26 in Johnson County, but it is 20.29 in Coffey County, and a few others are higher.

Assuming property taxes are allocated proportionally across counties to fund municipal services, the sales tax multiplier can be applied to existing sales tax rates to estimate the rate needed to replace property taxes. The calculations are based on 2025 tax data from the Kansas Department of Revenue.[i]

Table 2 shows the current local sales tax rate in Medicine Lodge (Barton County) is 2.75%: 0.75% for the city, plus a 1% county rate and a 1% special district tax. The local rate of 2.75%, times the 7.691 multiplier, would bring the combined local sales tax rate to 21.15%, plus another 6.5% for state sales tax, for a total of 27.65%.

The 2% local sales tax in Burlington (Coffey County) would increase to 40.58%, and the total, including the state sales tax, would be slightly over 47%.

Cities with Community Improvement Districts (CID) and other economic development subsidies would have significantly higher sales tax rates than in other parts of the city. The local sales tax rate in Wichita would increase from 1% to 2.77%, while the rate within the Delano CID would rise from 3% to 8.3%.

The actual rates needed may be higher to account for shifts in economic behavior. For example, food is still subject to local sales tax in Kansas, so some people in Pleasanton may shift their grocery shopping to Missouri to avoid a food sales tax rate of almost 22%.

What’s more, these higher sales tax rates only cover the $3.5 billion in property taxes used by cities, counties, and other municipal entities in 2025; eliminating property taxes for K-12, community colleges, and other educational institutions would have required an additional $2.9 billion in sales tax to offset taxes from 2025.

Given the nature of the state’s school funding formula and the wide disparities in property tax revenues that can exist even within counties, it makes more sense to increase the state sales tax rate to eliminate education property taxes than to raise local rates. At nearly $11 billion, the State General Fund would have to be cut by 27% to cover the $2.9 billion in education property taxes, making a sales tax increase the more likely option legislators would consider.

Total state sales and use tax generated $3.475 billion in FY 2025 at a rate of 6.5%, or about $535 million for each 1% of tax. Accordingly, the state sales tax rate would go from 6.5% to 11.9% to eliminate education property taxes and push the total rate above 30% in some communities.

A combined rate of 20% could be a non-starter in many parts of the state, let alone 30%, which would force other difficult choices. One option is to eliminate blanket sales tax exemptions for groups such as non-profit hospitals, churches, and other charitable entities. Another option is to lift exemptions for specific purchases, such as personal and professional services or prescription drugs, or to increase taxes on lottery and gaming.

Reducing reliance on property taxes for schools and local government

Another way to mitigate the impact of eliminating the property tax is to reduce reliance on it to fund local government services through state-mandated consolidations and other cost-saving measures.

Consolidation is certainly a controversial topic for some, but voters are supportive of the general concept.

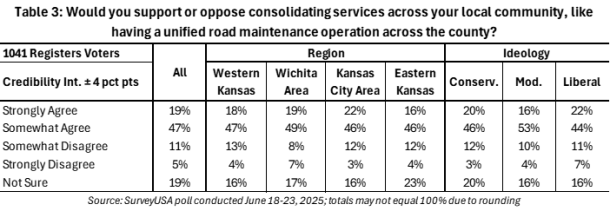

Our June 2026 public opinion survey shows 66% of voters support consolidating services across their communities, and only 16% are opposed. Further, their support is consistent across geographical and ideological boundaries.

From a taxpayer’s perspective, consolidating government entities or services is arguably the best option to reduce the property tax burden, given that Kansas is massively overgoverned.

Here are just a few examples from our annual Green Book analysis:

- Kansas is the 2nd-worst state in the nation for local government employees per capita.

- Kansas has 1,994 cities, counties, and townships with an average of 1,493 residents per entity. The national average is 8,806 residents per entity.

- Kansas has 34% more local government employees per capita than the national average and 52% more state government employees per capita than the national average.

Education employs many local government employees and is also inefficiently organized, with 285 school districts. The average Kansas school district has about 1,600 students, whereas several states have two to four times as many students, including Colorado, Texas, North Carolina, and Utah. The Kansas average falls below 1,000 without the counties of Johnson, Sedgwick, and Wyandotte.

Kansas would have about 37,000 fewer local government employees if staffing were at the national average. If the average cost of pay and benefits for those extra employees were just $75,000, taxpayers would spend $2.8 billion less on taxes to support local government employment – almost enough to eliminate education property taxes.

Kansas has 105 counties because, at its founding, it was decided that the county seat should be no farther away than a day’s ride on horseback. Citizens could be served today by far fewer county governments, making county consolidation one option for reducing costs.

Other consolidation options to reduce costs without cutting necessary services include:

- Eliminate municipalities below a certain threshold and have county governments provide services to those residents.

- Have one school district per county, except in counties with a population above a certain threshold.

School district consolidation raises understandable concerns about students having to travel long distances, but the one-district-per-county concept has long existed in 23 Kansas counties, so it can be done.[ii]

Sumner County, on the other hand, has seven districts serving about 3,000 students. That means taxpayers are paying for seven of everything: district offices with payroll, accounting, human resources, and IT, as well as duplicative managers and support staff for many other functions.

An alternative to consolidating school districts is to consolidate all non-instructional services into existing regional service centers that already provide some school district services. In addition to substantial savings, this approach allows superintendents to focus on improving student outcomes.

Variations on this concept also apply to other local government services. For example, technological advancements could allow functions like Recorder of Deeds or even property appraisal to be state-provided services rather than 100 or more of each at the county level. The state of Massachusetts undertook such consolidation in the late 1990s. Only five of the state’s 14 counties have active regional governments; some services became state-provided, and services in the other counties rely on municipalities for local services.[iii]

Each of these options, as well as replacing property taxes with sales tax, raises understandable concerns and questions that must be explored with citizens. The framework within which each should be considered is not whether it is a good idea, but whether the potential downsides are a worthwhile tradeoff for substantive property tax reform.

A $7 billion property tax tab cannot be reduced or eliminated without some combination of raising another tax, eliminating sales tax exemptions, or reducing the size of local government. The ideal taxpayer-focused approach would be to start by reducing local government spending through consolidation, next, decide which (if any) sales tax exemptions to eliminate, and then determine how much shortfall remains to be offset with additional sales tax revenue.

_________________________________

[i] Kansas Department of Revenue Statistics, calendar year 2025, City/County Annual Local Sales Tax and City/County Use Tax.

[ii] Kansas Department of Education, school enrollment report.

[iii] Massachusetts Basic Information, U.S. Census