Virtually every member of the Kansas Legislature says they support property tax relief, but there is a bipartisan effort behind the scenes to kill it. The reasons vary, and some are unspoken (allegiance to local government, the proposed legislation isn’t their idea, etc.), and the objections are mostly based on false or unproven claims.

The session began well, with the House and Senate leaders and the chairs of their tax committees coming together on an overall strategy: the House would work on a mill rate/revenue increase limit, and the Senate would focus on limiting the increase in assessed values. That continues to be the case, and it’s an efficient effort to pass both limits. Unfortunately, some Democrats and Republicans in both chambers are trying hard to kill one bill, hoping that that stops both from passing, and they aren’t letting facts and voter sentiment get in their way.

The need for assessment and mill rate limits is painfully obvious:

- Local officials use valuation spikes to impose unaffordable tax increases: Over the last four years, the average homeowner saw a 40% valuation spike, and while mill rates declined a tad, taxpayers still got a 32% property tax increase.

- Property taxes are much higher than necessary: Local property taxes would total about $4 billion if adjusted for inflation and population growth since 1997, but Kansans are paying $6.8 billion.

- Some taxpayers get unaffordable tax increases even if local officials barely raise property tax revenue: In 2024, Seward County, the City of Liberal, SUSD 480, and Seward County Community College reduced mill rates to collectively impose about a 1% tax increase, but someone who got a 15% valuation increase still had a 13% property tax jump.

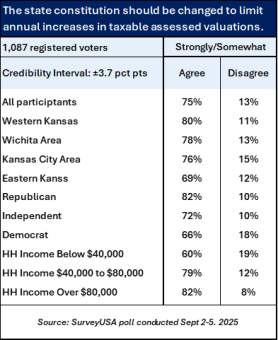

Over 80% of voters want an assessment limit, and 75% want a mill rate limit: Even the majority of Democrats and Independents want to vote on a constitutional amendment to limit assessed value increases, yet most Senate Democrats and three Republicans voted against the assessment limit. The House hasn’t voted on the assessment limit, but so far, House Democrats remain universally opposed, as do several Republicans.

Over 80% of voters want an assessment limit, and 75% want a mill rate limit: Even the majority of Democrats and Independents want to vote on a constitutional amendment to limit assessed value increases, yet most Senate Democrats and three Republicans voted against the assessment limit. The House hasn’t voted on the assessment limit, but so far, House Democrats remain universally opposed, as do several Republicans.

Here’s a recap of the most common bipartisan attempts to kill the assessment limit:

Myth #1: A constitutional amendment isn’t necessary to do an assessment limit.

As explained by Assistant Revisor of Statutes Amelia Kovar-Donahue during a Senate Tax Committee hearing, the Kansas Constitution requires that all property is taxed on a uniform and equal basis (subject to specific stated exceptions, of which an assessment limit is not included).

Newly constructed homes would be taxed based on the purchase price (and then subject to an assessment limit), which is a different basis than existing homes. Examples like this would violate the existing uniform and equal clause, so the constitution must be amended to add an assessment limit to the list of exceptions.

Myth #2: Taxes aren’t reduced, just shifted to other people.

Our analysis shows that had a 3% assessment limit gone into effect in 2005, residential and commercial property taxes would have been $1.7 billion lower, and ag land owners would have saved $1.3 billion. We allowed mill rates to increase five times more than they did over that period.

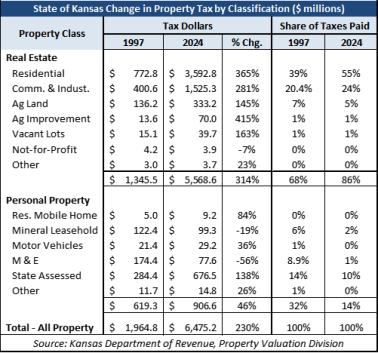

An assessment limit would stop the shift that’s been underway for many years. Residential property and mobile homes went from paying 39% of the property tax burden to 56%, while every other category paid a smaller burden. Ag dropped from 8% to 6%. Commercial and Industrial real estate, plus machinery and equipment, collectively dropped from 29% to 25%. State assessed and mineral leasehold each dropped by 4%.

Myth #3: Local governments will just raise mill rates to offset valuation reductions.

First, their desire to raise mill rates is a reason to vote for a mill rate limit, not an excuse to oppose an assessment limit. Back to where this column started, both an assessment limit and a mill rate limit as well as separate legislative chambers, work in tandem to protect taxpayers.

The average mill rate increased by just 9% over the last 20 years (2004-24). Had a 3% assessment limit been in place over the period, the average mill rate would have had to be 82% higher to produce the same property tax revenue in 2024. After years of claiming they didn’t raise taxes because the mill rate didn’t increase, local officials would suddenly have to justify big property tax jumps. We’ve already seen how the revenue-neutral transparency prompted many local officials to hold revenue-neutral and not increase property taxes, so it’s reasonable to believe that this additional transparency would have the same effect.

Myth #4: New home construction will be discouraged by an assessment limit.

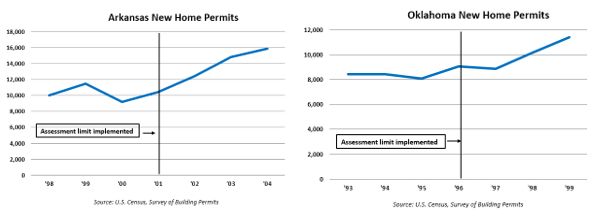

Assessment limits have existed in multiple states for decades, and if data proving they resulted in negative consequences existed, special interests would be citing it. Instead, they make unfounded claims of what might happen.

Arkansas implemented an assessment limit in 2001 and saw MORE new home construction. So did Oklahoma after its 1996 constitutional amendment. Oklahoma lowered the limit from 5% to 3% on residential property in 2012, and new home permits still increased.

Arkansas and Oklahoma built more new homes than Kansas on a per capita basis and as a percentage of existing housing stock in 2024.

Myth #5: Assessment limits create inequities.

The transferability clause in SCR 1616 eliminates inequities associated with home sales, as explained above.

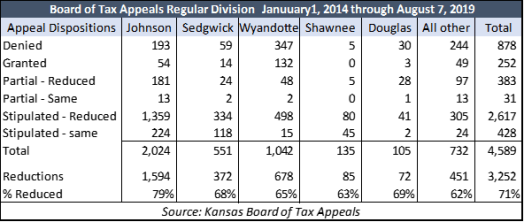

Those who give this reason for opposing an assessment limit also know that the current system is chock full of inequities. Just look at the volume of appeals.

The last time we checked, over 70% of cases that went to BOTA between 2014 and 2019 resulted in a reduction in value. That’s the hallmark of an unfair system.

Myth #6: The American Legislative Exchange Council (ALEC) opposes the assessment limit.

This one is a little inside baseball. Most Kansans have no idea what ALEC is, but referencing it here makes clear that some opponents of reform are just throwing things against the wall, hoping something sticks with legislators. They know people want an assessment limit, so they’re just trying to peel off a handful of legislators who are ALEC members.

Three legislators are falsely telling colleagues that ALEC opposes assessment limits. That’s not true because ALEC President Jonathan Williams told me they don’t take a position on SCR 1616, since it has no model legislation on the topic.

Still, Williams recently told me that the transferability aspect of the proposed assessment limit in Kansas addresses a fairness concern in other states’ legislation. SCR 1616 has a transferability clause that allows a property’s taxable assessed value to remain with it if sold or transferred, so the new owner pays taxes on the same assessed value basis as the previous owner.

Transferability avoids the fairness issue with assessment limits that reset when a property is sold. In those states, the newly-purchased home is paying more property tax than a similar home on the same street that has benefited from several years of assessment limits.

Conclusion

Legislators may not like some elements of an assessment limit, but that is true of most legislation they pass. It’s like considering the potential downsides to life-saving surgery; the patient must decide if the likely outcome is worth the risk.

In this case, the available data and information weigh heavily in favor of putting the constitutional amendment on the ballot and letting voters decide its fate, just as the patient decides whether to undergo surgery.

Local governments and some special interests are working hard to defeat SCR 1616, even knowing that that likely means taxpayers will get no substantive relief…again.

Taxpayers are suffering from property tax abuse, and a super-majority of them want a chance to vote on an assessment limit.

Here’s hoping that a few Democrats and Republicans will change their minds, and the House and Senate continue working together and let their constituents vote on SCR 1616.