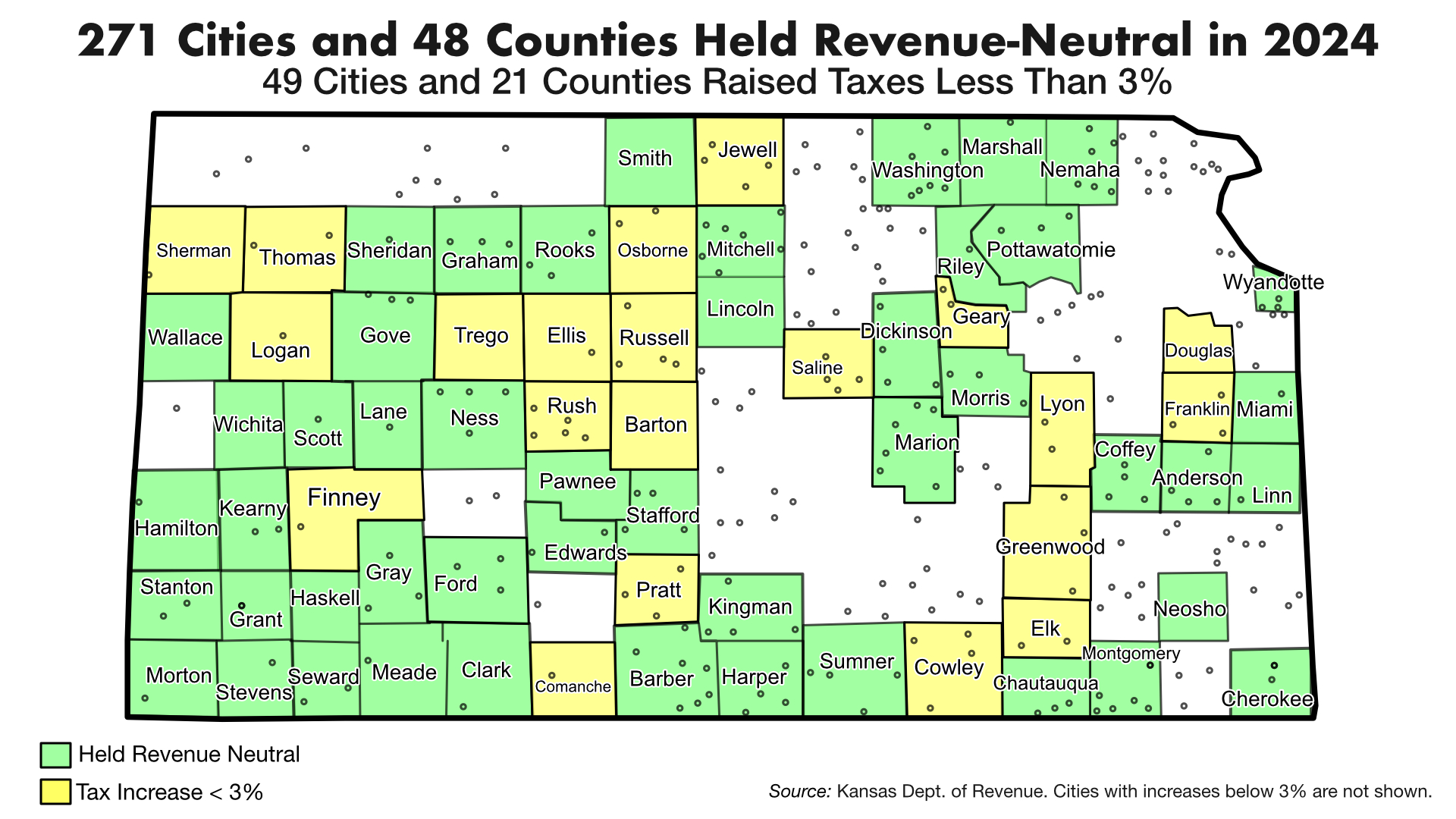

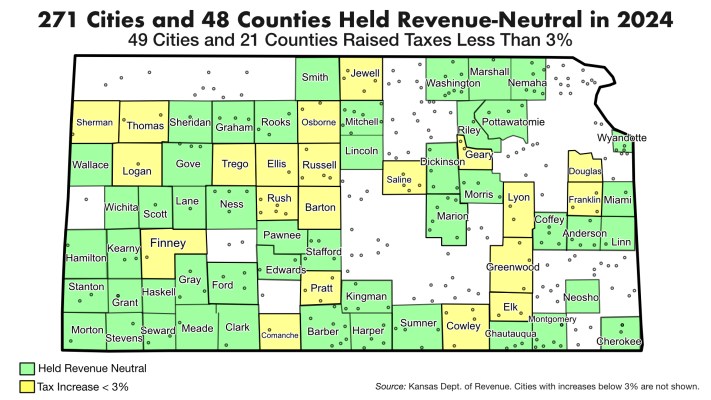

The American Legislative Exchange Council (ALEC) says the Kansas Truth in Taxation revenue-neutral system is the gold standard of state property tax transparency.

ALEC President and Chief Economist Jonathan Williams says, “At the root, unsustainable property tax increases are driven by local government overspending. As property values increase, local taxing authorities pocket the extra revenue from higher bills—whether or not there is any pressing need for it. Kansas has thankfully adopted Truth in Taxation which addresses that spending by requiring transparency and accountability. ALEC has adopted the Kansas model of Truth in Taxation as model policy, since it is the gold standard of state property tax transparency efforts. In 2024, this meant 62% of taxing authorities in Kansas did not increase property taxes.”

The revenue-neutral system in effect since 2021, has amazingly encouraged 49 counties, 271 cities, a few dozen school districts, and hundreds of other taxing authorities not to raise property taxes in 2025. Another 13% of local governments held tax increases below 3%, including 49 additional cities and 21 counties.

Unfortunately, some cities and counties still sock taxpayers with unaffordable property tax hikes, which is why legislators need to limit increases in assessed values and require voter approval of property tax increases greater than 3%.

82% of voters want to vote on tax increases, and 75% want the assessment limit. A large majority of Democrats, Independents, and Republicans support both measures, and Williams encourages legislators to take heed.

“Excessive property tax burdens drive the affordability problems many are facing today. ALEC also encourages lawmakers to explore other ways to address the unsustainable growth of property taxes with limits that are meaningful in the long term and avoid distorting real estate markets.”

Williams told me in a phone conversation that the transferability aspect of the proposed assessment limit in SCR 1616 is a unique way of addressing fairness concerns associated with assessment limits in other states.

Kansas Policy Institute fully supports SCR 1616. As explained here, the property tax cap in HB 2745 is not favorable to taxpayers, but it could be amended to reinstate revenue-neutral and, with a few other adjustments, be a great companion to SCR 1616.