Yesterday, I explained the complex process by which those property tax payments which hammer affordability for Minnesotans are calculated. This clarity reveals an important truth about property taxes.

The spending is the problem

The great secret of property taxes is that increases in property tax burdens are not driven by increases in property valuations but by increases in local government spending.

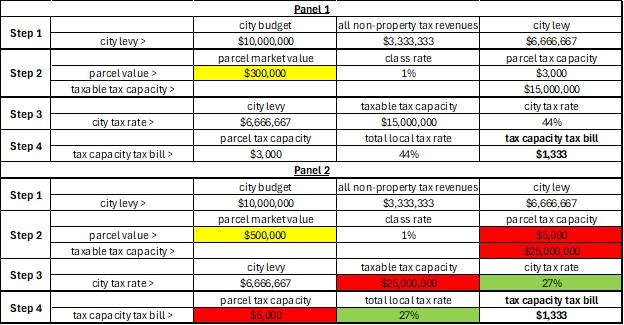

To see why, compare panels 1 and 2 in Table 1, which is a version of where we ended up yesterday.

Panel 1 shows the property tax payment — “tax capacity tax bill” — for a hypothetical city with a budget of $10 million, one third of which comes from “non-property tax revenues,” and which has 5,000 properties worth $300,000 each, the “parcel market value.” The property tax payment for each property is $1,333.

Panel 2 shows the property tax payment for exactly the same city except that each property is now worth $500,000. Because the average property is worth more the “parcel tax capacity” and “taxable tax capacity” — the city’s total tax base — are higher than in Panel 1, highlighted in red. But the “city levy” is the same so, spread over a larger tax base in Step 3, it gives a lower “city tax rate” than Panel 1, highlighted in green. And, because of this lower tax rate, even with the high “parcel tax capacity,” Step 4 gives us the exact same property tax payment as in Panel 1; $1,333.

In short, higher property valuations mean a higher tax base but a lower tax rate.

Table 1: Hypothetical property tax calculations

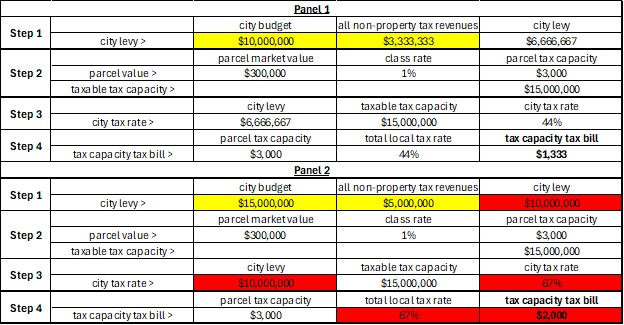

Look what happens, by contrast, when we increase the “city budget” between Panels 1 and 2 in Table 2 (assuming that one third of revenues are non-property tax in both scenarios). The “city levy” goes up, highlighted in red, but the tax base remains the same so the “city tax rate” goes up in Step 3. And this higher rate applied to the same “parcel tax capacity” in Step 4 gives us a higher property tax payment of $2,000.

Table 2: Hypothetical property tax calculations

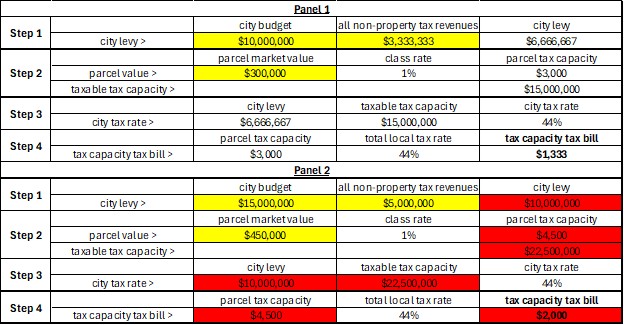

In truth, what usually happens is some mixture as shown in Table 3. Here we have the same increase in the city budget between Panels 1 and 2 as in Table 2, but we also have an increase in the average property value — or the assessor’s judgement of it, at any rate — from $300,000 to $450,000. This pushes up the “parcel tax capacity” and the tax base so that the “city tax rate” remains the same in Step 3. And, as a result, Step 4 sees the same tax rate applied to a the higher “parcel tax capacity” to give a higher tax bill of $2,000, the same as we derived in Table 3 by hiking government spending. The difference is that in Table 3, this showed up in a higher “total local tax rate” whereas in Table 4 it shows up in the higher valuation. The result is the same; a higher property tax payment resulting from a hike in government spending.

Table 3: Hypothetical property tax calculations

So, if you’re wondering why your assessed property value shot up when sale prices didn’t, this is why. The rise in valuations isn’t a cause of your increased property tax payment, but a consequence of the real casue, the increase in local government spending.

Hiking assessed property values enables local governments to finance spending increases without hiking tax rates, or without hiking them by the full amount necessary. The results, for the taxpayer, are the same, a squeeze on affordability.

What can we do about this? That is what we look at next.