The Kansas Legislature concluded its work of the regular session last week amid considerable controversy over an assessment limit that would protect people from unaffordable property tax increases resulting from appraisal increases of 20%, 30%, or even higher.

Earlier in the session, the Senate passed a proposal establishing a 3% annual assessment limit, with a 2022 base year. The House passed an alternative approach using a rolling average of valuation changes over multiple years, with several key elements left for the Legislature to establish in the future, including when the rolling average would take effect and how many years to include in the average.

As negotiations progressed this year, various compromise proposals were discussed, including fixed limits ranging from 7.5% to 10%. A conference committee ultimately agreed to a 9% fixed limit.

The House voted it down 59-63, far short of the 84 votes needed to put a constitutional amendment on the ballot. Some opponents were upset that their rolling-average concept wasn’t included, and others opposed any form of limit on assessed values. Most of the remaining members wanted the rate to be different; some wanted it higher, and others wanted a lower fixed rate.

At the time, it was not widely understood that a 9% limit was not the Senate’s original position; House negotiators had initially proposed a 10% limit and ultimately agreed to 9% during negotiations. The Senate, by contrast, has been consistent in supporting a 3% limit in prior proposals, and the movement to 9% reflected a conference effort to identify a proposal that could advance in the House.

There is still time to pass an assessment limit when the Legislature returns next week for its last few days of the year, and another option addresses the primary concerns of legislators who want to protect taxpayers from unaffordable jumps in assessed valuation.

A simple solution for legislators who truly want to help taxpayers

The House wants a rolling average on each piece of property with no limit, whereas the Senate wants a fixed rate that is predictable and provides much more protection to the taxpayer.

A few legislators are considering a different approach in hopes of reaching a taxpayer-focused compromise that uses elements of the House and the Senate positions: make the annual change in all assessed property the basis for the rolling average rather than a separate average for each piece of property. This retains the rolling-average feature and places the limit within a range slightly higher than the Senate’s 3% preference but considerably lower than the House’s.

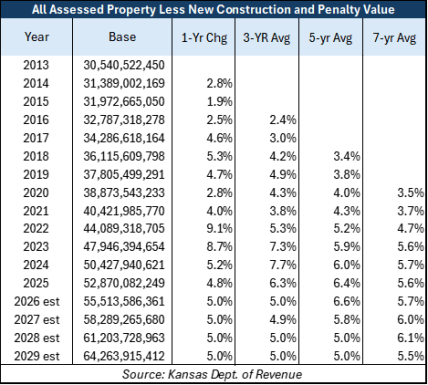

The total assessed value of all real estate and personal property, less new construction and penalty values, is shown in the Base column of the adjacent table. The change in the Base is shown in rolling averages of 3, 5, and 7 years, including the current year.

The total assessed value of all real estate and personal property, less new construction and penalty values, is shown in the Base column of the adjacent table. The change in the Base is shown in rolling averages of 3, 5, and 7 years, including the current year.

For example, the 7-year average of 3.5% shown for 2020 is an average of the changes from 2014 through 2020.

The highest historical annual change was 9.1% in 2022, and the multi-year averages are generally between 3% and 6%.

This concept can be implemented in 2027 if voters approve it this year, and it is much easier for County Treasurers to implement, with a single average applied to all parcels rather than a couple of million averages for individual parcels.

This concept contains the key elements of the House and Senate positions and, most importantly, it protects property owners from double-digit valuation hikes that lead to unaffordable tax increases.

Assessment limit opponents say local officials will respond by jacking mill rates to offset the valuation limits, but that is mitigated by the mill rate limit both chambers passed last week. The Senate passed it by a vote of 22-18, and the House by a vote of 63-59. HB 2745 allows voters to sign a protest petition against property tax increases that exceed the rate of inflation; if the petition succeeds, the taxing authority must stay at revenue-neutral and not raise taxes at all.

Voters prefer a fixed, low assessment limit

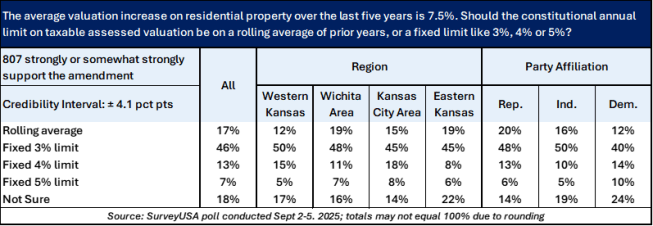

Public opinion is very clear: 75% of Kansas voters want an assessment limit. Asked what kind of limit they prefer, 17% say they want a rolling average, 66% want a low fixed-rate limit, and 18% are undecided.

The House’s preference for a rolling average contradicts voters’ desire, but if they can’t get the votes to agree on a low fixed limit, a rolling average of the change in all property at least puts the limit near the lower range voters want.

A rolling average on each piece of property isn’t worth much to someone who consistently receives double-digit appraisal increases. At best, it just spreads the pain a little, whereas a fixed low rate prevents it, meaning property owners pay higher taxes with a rolling average for each property than under the compromise plan, which averages the change across all properties.

This common-sense compromise doesn’t give voters exactly what they need, but it’s reasonably close and much better than another year without protection from double-digit valuation hikes and property tax increases.

Resolving these policy issues isn’t difficult. Overcoming the unspoken differences is another matter, however.

Real relief vs. the appearance of supporting an assessment limit

Every legislator said Kansans need property tax relief at the beginning of this session, but that doesn’t mean the same thing to everyone.

To some, property tax relief cannot cause those that created the property tax crisis – cities, counties, and school districts – to operate more efficiently. Instead, they would have the state issue rebates or require business owners to pay more so that homeowners can pay less.

Other legislators worry about getting crosswise with influential agricultural lobbying groups, as well as cities, counties, and school districts.

Some opponents, including legislators, cite easily refuted objections or illogical claims to justify their opposition. For example:

- They claim that assessment limits will shift the tax burden, yet they provide no evidence of that happening in the states that have had assessment limits for decades.

- They fear an assessment limit will discourage new home construction. They provide no evidence to support their claim, but we found data showing the opposite: new home construction increased following the implementation of assessment limits in Arkansas and Oklahoma.

- House members who voted for a rolling average of an unspecified number of years, and with no start date, said taxpayers will reject a fixed flat rate limit that starts immediately because it’s too hard to understand.

- They cite a national policy group that cautions against assessment limits due to fairness concerns, even though the Kansas version addresses this by allowing the assessment limit basis to remain with the property when sold.

Legislators understand that failing to pass an assessment limit means taxpayers will continue to suffer double-digit valuation and property tax increases. The question each must answer is whether their concerns about the potential side effects of an assessment limit justify allowing the suffering to continue for many of their constituents.