When Gross Domestic Product (GDP) shrank in the first quarter, many commentators were quick to blame the Trump administration. When GDP surged in the second quarter, many other commentators were quick to credit the Trump administration. Both sides were overstating their case.

First, What is “What is GDP?” As I wrote in May:

To quantify domestic production of goods and services, GDP measures spending and this typically falls into four categories: personal consumption expenditures (C); gross private investment (I); government purchases (G); and net exports (X – M), composed of exports (X) minus imports (M). If you’ve studied macroeconomics at any level, you’ll probably recognize this equation:

GDP = C + I + G + (X – M)

To the layperson, this might suggest that we would be better off with a lower level of imports:

That, after all, is what the GDP equation above seems to say: Imports (M) are subtracted. If you spend $45,000 on an imported car, the equation seems to imply that $45,000 should be subtracted from GDP.

But GDP is trying to measure domestic production, so imports — foreign production — should not be counted towards GDP. So, if you spend $45,000 on a foreign car that shows up in “Personal consumption expenditures,” but it is not domestic production so it has to be removed from GDP by subtracting the $45,000 in the “Exports” category. It is a question of accounting.

And, if a business buys a foreign car, that shows up in Investment.

As I noted in July regarding the second quarter figures:

…whereas in the first quarter of 2025 Investment surged and so did Imports — a negative, remember — and that explained the changes in GDP, in the second quarter it is different: Now we have a decline in both Investment and Imports with the former pushing GDP down and the latter up.

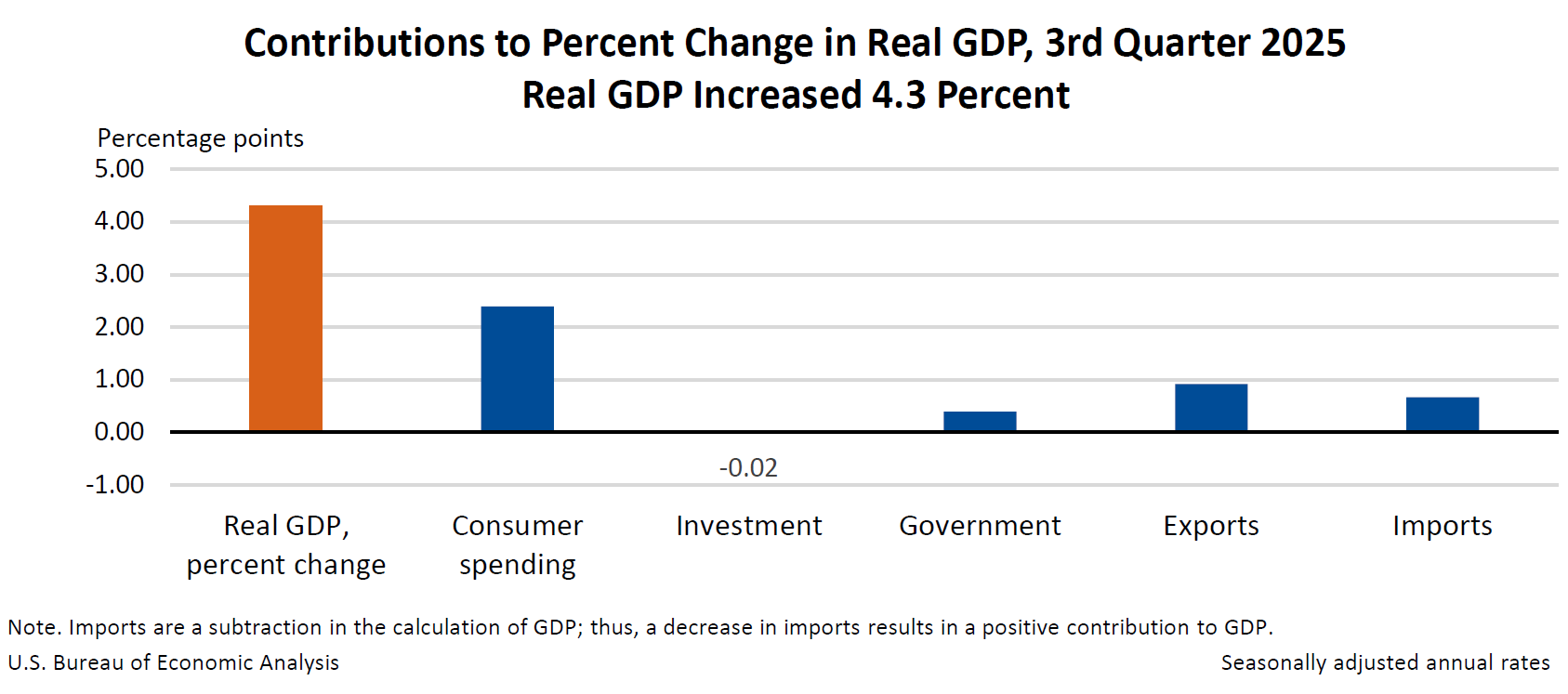

I noted that “[t]hese swings in Investment and Imports in the last couple of quarters are unusual” and, indeed, they have not been maintained. Today, the Bureau of Economic Analysis (BEA) reports that: “Real gross domestic product (GDP) increased at an annual rate of 4.3 percent in the third quarter of 2025 (July, August, and September)…”

The increase in real GDP in the third quarter reflected increases in consumer spending, exports, and government spending that were partly offset by a decrease in investment. Imports, which are a subtraction in the calculation of GDP, decreased…

Compared to the second quarter, the acceleration in real GDP in the third quarter reflected a smaller decrease in investment, an acceleration in consumer spending, and upturns in exports and government spending. Imports decreased less in the third quarter.

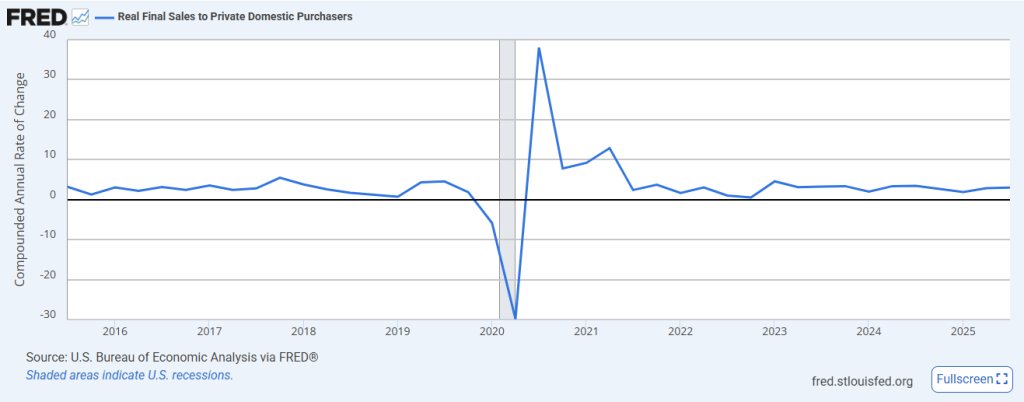

I have referred previously to “Real final sales to private domestic purchasers,” a sort of “core” GDP. The BEA reports that this: “increased 3.0 percent in the third quarter, compared with an increase of 2.9 percent in the second quarter.” Indeed, it compares with an average of 2.8 percent from Q3 2015 to Q4 2019 and 2.7 percent from Q3 2021 to Q2 2025, as Figure 1 shows.

Figure 1

For all the fuss about the macroeconomy, so far it is a case of “Steady as she goes.”