by Tyler Watts, Ph.D.

We free-market economists tend to pooh-pooh complaints about income and wealth inequality. When “democratic socialist” or even populist right-wing demagogues complain about stagnant or declining middle-class incomes, we point out all sorts of empirical flaws in the data they use: “They don’t include government transfer payments in income measures.” True. “They don’t include the monetary value of benefits like health insurance.” Often true. “They don’t account for the fact that almost everything has become less expensive in work-time cost.” True. However, just stating that, “actually, lower- and middle-income people are better off than ever” is cold comfort for people’s felt economic anxiety. Most people compare their personal situation to what they currently see or read on their screens, not to a detailed breakdown of economic stats. Perceptions matter in politics, and a growing body of people feel that “the system is rigged” in favor of a small cadre of elites, at the expense of the broader population of working schmucks. Even if these complaints are baseless, or at best shallow, they carry political heft — vis. Bernie Sanders, Zohran Mamdani, AOC, and the like, with their redistributionist tax-and-transfer schemes, largely aimed at leveling those dreaded inequalities. To preserve and protect future economic prosperity, we’d better take this issue seriously and tackle it strategically, lest we lose it all to the utopian redistributionist dreamers.

It seems that the pro-capitalist coalition (conservatives, libertarians, and normal people) can offer one of two main answers to economic inequality. We can go with pure Ayn Rand ideology: capitalism is a meritocracy, the rich earned it, profit seeking generates socially beneficial innovation, and so on — so stop complaining, work harder, and leave me alone. Or we can try a slightly different tack, call it the “populist capitalism” response: If workers don’t like being left in the dust by capitalists, why don’t we do everything we can realistically do to make those workers into also-capitalists? In other words, let’s enact broad policy measures to graft as many people as possible into the ownership structure of the economy — let’s make them all capitalists. When more people have income from working but also own a piece of the economy’s capital assets through the stock market, they too will earn a share of capital’s income and become real stakeholders in the free market economic order. These worker-capitalists will more likely be on guard against bad socialist policies, like wealth taxes, redistribution schemes, socialized healthcare, and so on — policies that deter investment, sap incentives to work and innovate, erode growth, and make everyone poorer.

There are signs that populist capitalism is gaining ground. More Americans than ever, particularly younger folks, are investing in the stock market, and well over half of US workers participate in workplace retirement investment plans. We have seen growing numbers of “401(k) millionaires” — i.e., middle class earners who built wealth quietly over decades through disciplined contributions to their tax-advantaged funds.

Building on this momentum, Congress, President Trump and Treasury Secretary Scott Bessent have taken a great step towards massively broadening capital ownership with the new Trump Accounts. Think what you will of their orange namesake, Trump Accounts can become a vehicle to create full-fledged capitalists out of America’s next generations. Essentially kiddie IRAs, Trump accounts can be opened for any child at birth. Family, friends, and employers may contribute up to $5,000 annually, with the requirement that funds be invested in an automatically-diversified portfolio of stock index funds. Each child gets ownership of his/her fund at age 18, when money can be withdrawn without penalty for certain qualified expenses like college or a home down payment. Otherwise, Trump Accounts convert automatically to traditional IRAs, to which the account holder can keep contributing all through his/her working years. Well-funded Trump Accounts can and will be a vehicle to massively jumpstart young Americans’ retirement savings.

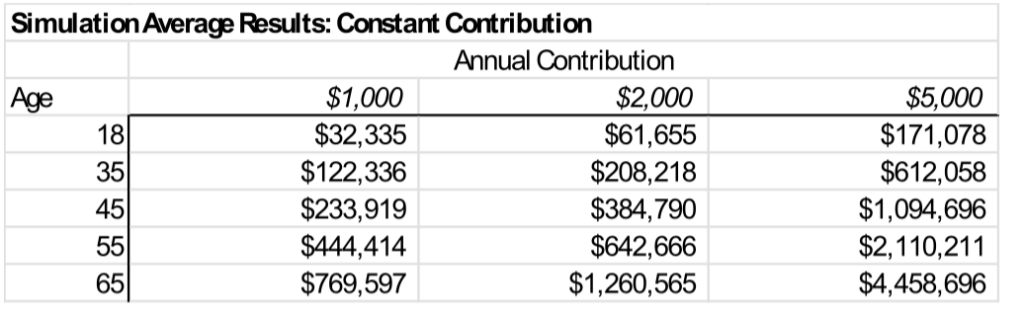

To show the potential of Trump Accounts for lifetime wealth building, I set up a spreadsheet simulation to model potential investment results. I assume investing strictly in an S&P 500 index fund, and I maintain the same annual contribution level for the life of the account holder. For each yearly contribution amount, I ran 100 trials, applying a rate of return drawn at random from historical S&P 500 data: with an average annual real (adjusted for inflation) portfolio return of 6 percent (reinvesting dividends), and standard deviation of 20 percent.

Continual yearly contributions to a Trump Account will grow nicely over 18 years, potentially reaching well into 6-figure territory. Continuing contributions for the account holder, even at laughably modest yearly amounts for an average income earner, should easily reach 7 figures well before retirement age. In scenarios in which contributions grow with income (a more likely situation for well-informed, responsible capitalists), we are looking at a proliferation of American millionaires “like no one’s ever seen before” as the President himself might put it.

In addition to creating new generations of “birthright capitalists,” funded Trump Accounts, upon maturation into turbocharged IRAs, may very well provide an exit ramp from the Social Security debacle. As sober economists know, Social Security is a fiscal train wreck in slow motion, a “paygo” system that hands current workers’ tax contributions directly to today’s retirees, with no real investment or accumulation of returns in between. Social Security has paid out more than it takes in since 2010, and the so-called trust fund—IOUs for prior years’ surpluses that Congress blew on other spending programs — is expected to run dry by 2033. If Social Security is not reformed—i.e. some combination of increasing retirement age, boosting payroll taxes, or trimming benefit formulas — the “Old Age” (retirement) program will pay out less than 80 percent of scheduled benefits to seniors once the trust fund is depleted. If, however, we can massively jump-start future generations’ retirement accumulation with Trump Accounts, Social Security reform can become much more viable when it will be needed most. We can transition Social Security into a means-tested welfare program for truly poor old folks. Better yet, we can phase out Social Security altogether, as it won’t be relevant for most worker-capitalist-investor Americans, thanks to the compounded gains on their Trump Accounts.

Americans have had a long and fruitful love affair with the stock market, but until fairly recently, building lifetime wealth through stock investing was mostly the province of tycoons, trust-fund kids, and white-collar elites. The creation of tax-qualified, defined-contribution retirement plans like IRAs and 401(k)s enabled tens of millions of Americans to tap into to the largest engine of individual wealth creation in human history. With Trump Accounts, we can truly democratize this wealth-building machine at mass scale, and take giant steps toward socialism-proofing the world’s richest and most innovative economy. This is an idea we probably should have done 20 or 30 years ago, but better late than never. Now that Trump Accounts are here, let’s take advantage of this wonderful opportunity to pass down our great economic legacy to all our posterity. Make a Trump Account contribution for a child you love today.

Tyler Watts, Ph.D., an adjunct scholar of the Indiana Policy Review Foundation formerly with Ball State University, is professor of economics at Ferris State University.