Discussions about balancing government budgets inevitably prompt elected officials to ask taxpayers, “What service would you cut?” Regardless of intent, that tactic implies that government spending cannot be reduced without cutting services, and that seems to be the purpose of a public opinion effort on the USD 259 Wichita budget.

Some taxpayers living in the Wichita school district received an email last week from Wichita State University professor Dr. David Guo and University of Kansas Associate Professor Dr Zachary Mohr. The email said they are “conducting a budget simulation to gather citizen input on the budget and to better understand residents’ attitudes towards Wichita Public School District’s annual budget.”

We asked them to respond to these questions:

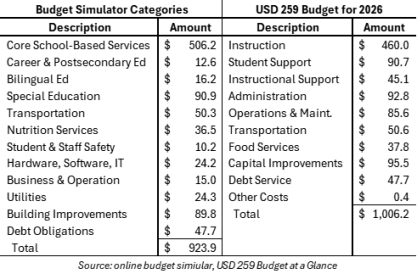

- What is the source of your data? Your categories total $923.9 million, but the district’s budget for the fiscal year just ended is $1,006.2 million

- Why are participants not given options to suggest efficiency opportunities? Options to increase or decrease by a specific dollar amount indicate that funding AND services would be reduced, whereas operating more efficiently saves money without compromising services.

- When will results be made public?

- Will these responses be used in the bond election campaign?

A “read” receipt was received from Dr. Guo, but neither professor responded to the questions.

Except for Debt Obligations, none of the spending numbers provided by Guo and Mohr matched the amounts from the 2026 Budget or any other USD 259 publication we could find. Most of the category descriptions are also different.

Except for Debt Obligations, none of the spending numbers provided by Guo and Mohr matched the amounts from the 2026 Budget or any other USD 259 publication we could find. Most of the category descriptions are also different.

The website says the listed expenditures result in an $8 million deficit, but there is no explanation of the spending assumptions that led to that outcome.

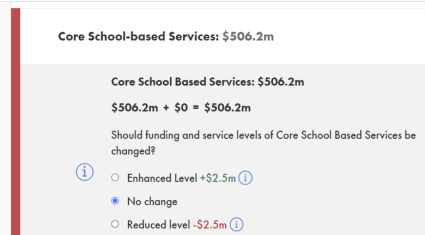

Users are given very few options to adjust the budget. For example, the options to adjust $506.2 million in Core School-based Services are to enhance or reduce the “funding and service levels” by $2.5 million.

The exercise is structured as though the district has no opportunities to reduce costs by operating more efficiently while providing the same services. A district with a $1 billion budget certainly has many opportunities to reduce discretionary spending and eliminate unnecessary positions without having to cut services.

The exercise is structured as though the district has no opportunities to reduce costs by operating more efficiently while providing the same services. A district with a $1 billion budget certainly has many opportunities to reduce discretionary spending and eliminate unnecessary positions without having to cut services.

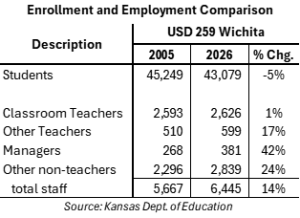

Enrollment for the year just ended is 5% lower than in 2005, but employment is 14% higher, and a lot of the growth is in non-teaching positions. There are 17% more special education teachers and 1% more classroom teachers, but the number of managers jumped by 42% and other non-teaching positions increased by 24%.

The Manager category includes the superintendent, assistant superintendents, principals, assistant principals, directors, managers, instruction coordinators, and curriculum specialists.

Prior school boards, no doubt, had good intentions in expanding staff. Still, student outcomes remain very low; 44% of students have a limited ability to read and only 29% are proficient…and that’s after the State Board of Education reduced performance standards to make outcomes look better.

Prior school boards, no doubt, had good intentions in expanding staff. Still, student outcomes remain very low; 44% of students have a limited ability to read and only 29% are proficient…and that’s after the State Board of Education reduced performance standards to make outcomes look better.

Adding 113 managers and 543 other non-teaching positions certainly hasn’t improved student achievement, so it makes sense to review staffing levels to balance the budget and get more resources into the classroom.

Just returning to the district’s 2005 students-per-manager ratio would eliminate 126 managers and, assuming average pay and benefits of $100,000, save the district $12.6 million. That more than covers the stated $8 million deficit with a single efficiency exercise…and there are many more opportunities.

Many districts, including USD 259, have unnecessary levels of operating cash reserves. These cash balances increased from about $460 million in 2005 to $1.33 billion last year.

USD 259 increased its operating cash reserves by about $100 million over the last 20 years, going from $75 million to $178 million, and that doesn’t include $187 million held for capital outlay and debt payments. Most of that $100 million increase represents state and local tax money that wasn’t spent in prior years.

USD 259 started the just-concluded school year with about 28% of its operating expense in cash reserves, whereas the average in Kansas is 19%, and even that level is unnecessary. We know this because dozens of districts operate each year with less than 12% in reserve.

3-bucket exercise reduces spending and preserves necessary services

Another budget tool taught by our Kansas School Board Resource Center is called the 3-Bucket Exercise.

School board members can work with the finance staff to separate expenditures into three buckets, with Bucket #1 containing all discretionary spending; the district isn’t required to spend the money, and it is not directly related to improving student outcomes.

Expenditures that are necessary to some extent and have an indirect impact on outcomes go into Bucket #2. Each district needs some degree of administration, and learning will suffer if the district doesn’t heat schools and provide other basic necessities. Student support services and instructional support services go in this bucket.

Bucket #3 holds expenditures directly related to improving outcomes and recorded in the Instruction function, as defined by the Kansas Department of Education. Generally speaking, these are costs associated with direct interactions between teachers and students, including instructional materials.

The purpose of the 3-Bucket Exercise is to understand priorities, and honesty is essential; board members must resist the temptation to load everything into bucket #3.

If the district has a budget shortfall, the board should remove spending from bucket #1 until the deficit is resolved. If a deficit still exists when bucket #1 is emptied, move to bucket #2 to reduce the cost of providing those services.

Improving student outcomes should be the district’s purpose for existing, which must be the basis for evaluating every dollar spent. Budgets should be built from the classroom out, but that’s not how most school district budgets are constructed in Kansas and across the nation.