Back in January, the Tax Foundation published their ranking of state corporate income taxes for 2026. As Figure 1 shows, with a corporate income tax rate of 9.8%, Minnesota ranked second after only New Jersey with its rate of 11.5%.

Figure 1

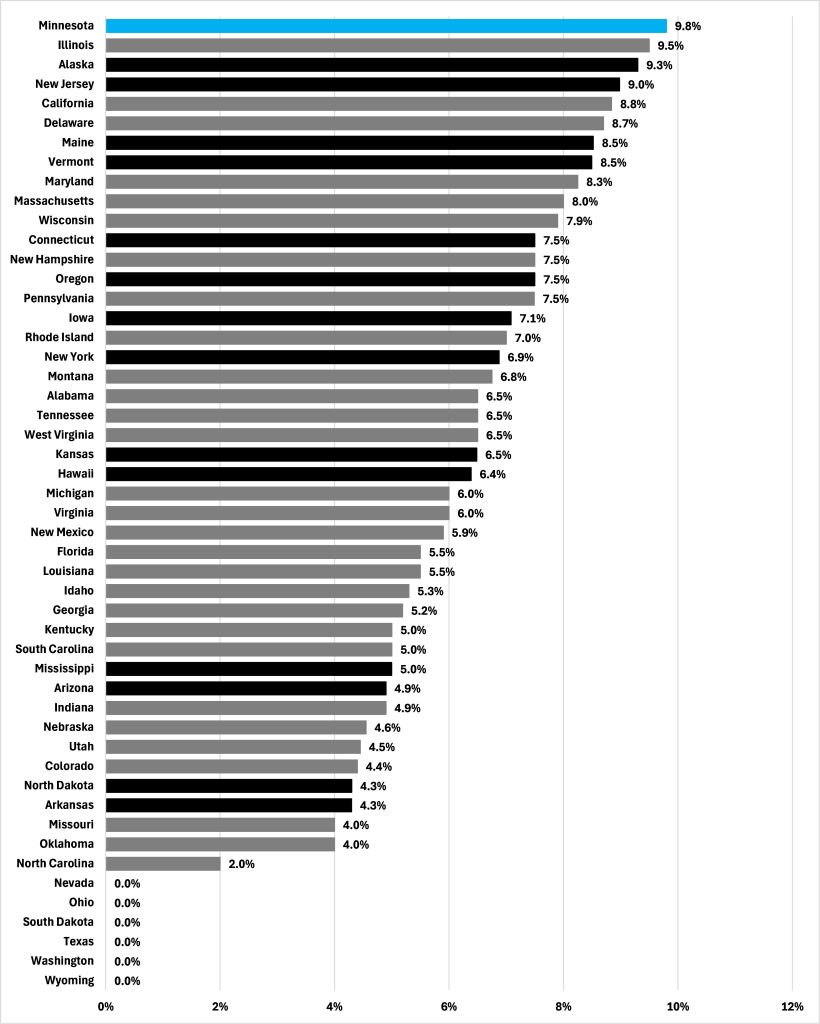

But New Jersey only imposes that 11.5% rate on net taxable income above $10 million annually; below that, the business is taxed at lower rates ranging from 6.5% to 9.0%. Minnesota, by contrast, imposes that rate of 9.8% on the very first dollar of net taxable income. So, while a business with $10 million of net taxable income in New Jersey will face a top rate of corporate income tax of 9.0%, in Minnesota it will face a rate of $9.8%. Indeed, for this smaller business, the effective tax rate — the actual percentage of net taxable income paid in tax — is higher in Minnesota than in any other state, as Figure 2 shows.

Figure 2: Effective tax rate on a business with $10 million net taxable income, 2026

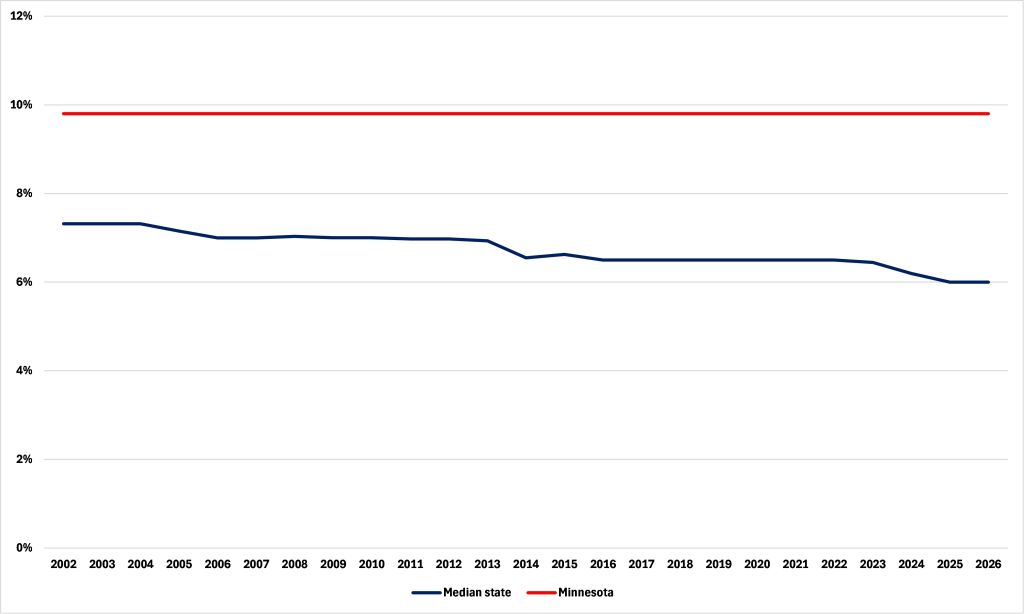

According to data from the Institute on Taxation and Economic Policy, Minnesota has had a corporate income tax since 1933, and its rate has been 9.80% since 1990. But while our rate might have remained the same, other states have either raised or lowered their corporate tax rates. Indeed, as Figure 3 shows, the effective corporate tax rate on a business with net taxable income of $10 million in the median state has fallen from 7.3% in 2004 to 6.0% in 2026. This has happened in three steps; 2004 to 2006, 2013 to 2016, and 2023 to 2025. It means that Minnesota’s effective corporate tax rate on such businesses has gone up relatively; our state’s rate was 2.5 percentage points about the median in 2004 but that was up to 3.8% this year.

Figure 3: Effective tax rate on a business with $10 million net taxable income

A couple of years ago, I testified in St. Paul and explained why the state government shouldn’t hike taxes to close its budget deficit. When I pointed out our state’s subpar economic performance and high taxes, it was suggested that taxes were high back in the days when the state’s economy was doing better so couldn’t be a factor. Perhaps they were, but, as Figure 3 shows, so were everybody else’s. It is not that Minnesota’s economic slowdown follows a hike in the state’s corporate tax rate but that it follows a relative hike as other states have cut theirs.

To what extent is the one phenomenon caused by the other? Watch this space.